Once upon a time there was a young commodities trader called Sanjeev Gupta who wanted to do good in the world and to get rich while he was at it.

Once upon a time there was a young commodities trader called Sanjeev Gupta who wanted to do good in the world and to get rich while he was at it.

He was very saddened by the harm being done to working class people in Britain by de-industrialisation and the relentless export of Britain’s manufacturing tradition to faraway countries, where production costs are low, just so greedy capitalists can boost their profits, build up their fortunes faster and buy ever more extravagant yachts and private planes.

However, he had always been taught not to sit and whinge but to get up and do something about it … so he did.

In the indomitable style of Don Quixote, he donned a metaphoric shaving basin on his head and sallied forth as a knight in armour to rescue Britain’s beleaguered steel business. Nothing could be simpler. He would buy up ailing plants, invest heavily in the most up-to-date technology in order to make them super-competitive, and provide work for thousands of honest, hardworking and skilled British people. Yes, of course it would be expensive – way beyond his means – but nil desperandum! Everybody knew that capitalists everywhere were falling over themselves to provide loans to people who would promise them a good return for their investment seeing as the world crisis of overproduction was making profitable avenues of investment very scarce on the ground: these capitalists would be glad to provide him with all the money needed, he would spend it saving jobs, and everyone would be grateful, as he got undying thanks from all the best and influential people, and made big, big money into the bargain (unlike poor old Don Quixote in this respect!).

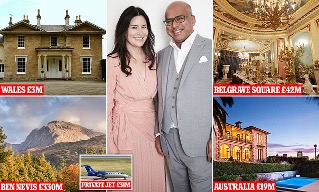

His adventures “began in 2013 when Gupta, then a trader of commodities, acquired a small steel mill in the Welsh town of Newport.

“The move saved the plant from permanent closure, setting the pattern for almost a decade of ceaseless dealmaking that won Gupta political support as he saved jobs in industries that had been written off …” (Sylvia Pfeifer, Oliver Barnes and Jamie Smyth, ‘Sanjeev Gupta’s empire building faces test of its steel’, Financial Times, 10 March 2021).

In a mere 7 years Don Sanjeev’s exploits proliferated in the most extraordinary manner. Not only were there far more industries in Britain that needed saving, but there were even more in other countries to attract his indomitable knightly exploits. Thus today “his UK businesses, … employ close to 5,000 people ….

“Its operations are spread across the UK, spanning a mill in Scunthorpe, an aluminium technologies car components centre in Coventry to Britain’s last aluminium smelter in Scotland. Its speciality steel business makes high-end products for aerospace manufacturers, including Rolls-Royce. The group also owns an estate in the foothills of Ben Nevis, Britain’s tallest mountain” (ibid.).

Abroad his bounty is even more impressive: his operations employ about 35,000 people across 30 different countries. “Gupta’s most strategically important asset is probably the Dunkerque aluminum smelter in France, which he acquired for $500 million in 2018.

“One of Europe’s biggest smelters, it’s a critical supplier to the region’s automakers…

“In his biggest deal, Gupta acquired seven steel sites for 740 million euro ($880 million) from ArcelorMittal in 2019. The largest were in Eastern Europe, including the Ostrava and Galati integrated mills in the Czech Republic and Romania.

“The buying spree … also involved assets in North Macedonia, Belgium and Luxembourg…

“Gupta’s Australian assets are among the most stable in his empire …The iron ore operations he owns in the Middleback Range supply the steel businesses he acquired in 2017.

“The Whyalla steelworks, about 400 kilometers (249 miles) north of Adelaide, is a crucial supplier of rail steel in the country. Gupta also owns InfraBuild, which remelts scrap metal and is a key supplier to the construction industry” (Eddie Spence, Thomas Biesheuvel and Jack Farchy, ‘Just how big and important is Sanjeev Gupta’s metals biz empire?’, Business Insider, 11 March 2021).

He has also ventured into the US and Germany.

Our valiant knight errant is undoubtedly proud of the fact that not only has he saved thousands of jobs all over the world, and been able to buy himself some impressive mansions, but his endeavours have supported various other essential local industries that employ even more people, having become an essential link in the supply chain for their various manufactures.

He has done so by single-handedly and indomitably confronting the dragon of Export of Capital by the simple device of diverting capital to himself by means of borrowing and then spending it on reviving struggling industries in rich countries, less deductions to support his own luxurious lifestyle, of course.

However, reality does not go away however much, like Don Quixote, one prefers not to take it into account. Borrowing has to be repaid and promises to lenders have to be fulfilled, which it was always unlikely our bold warrior was going to be able to do simply with the profits he was able to generate from taking over industries in their death throes. Undaunted, he kept going on and on – by the simple expedient of borrowing more and more, to buy more and to pay his creditors. But as the debts mounted this became more and more difficult, until this year his noble campaign finally ran into its inevitable fate – utter bankruptcy, dragging down not only himself but also his trusty fellow knight in shining tinfoil armour, Don Lex Greensill.

The struggle to stay afloat

Much of Gupta’s billions of pounds of borrowing were provided by Lex Greensill.

Lex Greensill is cast in the same mould as Gupta, willing to lend money he has himself borrowed to support excellent causes, such as those espoused by Sanjeev Gupta, without going through the expensive and time-consuming bureaucratic hoops supposed by ‘due diligence’ (i.e., checking that the borrower really will be able to repay with interest as he has contracted to do). In fact, Lex Greensill and Sanjeev Gupta were a marriage made in heaven. Greensill borrowed and lent to Gupta, Gupta spent on all his good causes. But Greensill had to keep borrowing in order to keep lending to Gupta the money he needed, but those he turned to were beginning to refuse him …

“…Lex Greensill, a cheerful chappie financier, left Morgan Stanley and turned up in Whitehall in 2011 saying that he had a whizz-bang idea that could help [the problem of the government not paying its bill promptly or even on time].

“Greensill was a proponent of supply-chain finance. He spun a yarn about the troubles his parents had experienced as farmers in Australia when big suppliers took an age to pay. The supply-chain finance firm could stand in the middle. How about applying this notion to parts of the British government, he asked his new friends in Whitehall?

“It’s not a terrible idea but in its broad principles this is just invoice factoring, a fairly mundane (in good times) practice that has been around in England since perhaps the 16th century. The supplier needing money gets the invoice paid quickly by the factor at a discount. The factor gets the full invoice paid later by the purchaser. The difference is profit.

“Greensill’s innovation was to flip the process, offering ‘reverse factoring’ [i.e., paying a debtor’s suppliers on time on behalf of the debtor in return for the debtor repaying him with interest] and taking his cut from government money. This way Greensill would get contracts from the government to pay out the money it owed, thus helping small business (which would get its money in full), the stated aim of ministers for decades. Interestingly, much of Whitehall resisted his offer of help, on the basis that the government should just pay its invoices quicker, with no need for a middle-man.

“Factoring may be mundane but it is risky. At some point, and it is difficult to know when, the credit cycle changes and invoices go unpaid as firms go bust. But Greensill had been clever. He had the backing of the British government, which never goes bust. This lent authority and the impression of solidity as he prepared to expand.

“And he had to expand. The problem was that he had created a model for a perfectly decent, modestly profitable factoring business with some government contracts. Nothing wrong with that in business terms, but it is not very exciting and certainly not a pathway to becoming a super-rich titan of global finance. Greensill wanted to fly around in private jets. At one point the company he created had the use of four.

“His company diversified and grew rapidly. It offered ‘future accounts receivables finance’. That means lending money to a firm even before it has sold something, on the promise of future payments once it does.

“Greensill Capital bought a bank in Germany, becoming a more conventional commercial lender, issuing notes, debt, that generated cash he could then lend on. …

“Through Credit Suisse, Greensill set up various funds for investment. The whole contraption was then insured, providing investors with confidence. All this was underpinned, remember, by the public relations mantra that something magical, capable of creating billions, had been created out of humble old factoring and invoicing.

“Here the whole mad scheme takes on a South Sea Bubble feel. Some of the biggest global investors piled in with hundreds of millions of pounds of capital. Alas, Greensill had really made himself into a bank. And as a student of financial crises, let me tell you there are few things more inherently frightening than banking when it goes wrong.

“Banking rests on conjuring up credit and playing with risk. The fundamental factors that dictate survival or destruction are age-old. How solid is the bank in an emergency? Who has the bank lent to and can they pay it back?

“There is always a moment in these stories when the tide suddenly goes out and we discover, in the old phrase, who is wearing swimming trunks and who isn’t.

“In early 2020, when Covid started to gum up the wheels of the international economy, Greensill was properly tested for the first time by a credit cycle going wrong. Insurers and lenders fled. Lex was revealed to be not wearing swimming trunks. Cue destruction” (Iain Martin, ‘Greensill’s fantasies lost touch with reality’, The Times, 5 April 2021).

It was because of government contracts that Greensill looked so solid, and it was because he looked so solid he was able to borrow money, which he could then lend to Gupta. But alas in turned out that he was not solid at all, so he and Gupta sank together.

However, before he sank nobody can say that Greensill did not struggle extremely hard. He was able to bring on board ex Tory Prime Minister David Cameron whom he set to work huckstering his friends and acquaintances in the present Tory government to secure Covid emergency funding with which he hoped to keep himself and Gupta afloat until the day they both hoped the clouds would roll by and they could both return happily to solvency.

Thanks to Cameron’s intervention – his enthusiasm no doubt bolstered by his share options in Greensill’s company that were worth tens of millions of pounds provided the company could be saved from collapse – Greensill was able to pitch his proposals to the Treasury and to civil servants at the highest level.

“The evidence so far is that Mr Cameron lobbied four government ministers on behalf of Greensill. These efforts secured a meeting between Mr Greensill and Matt Hancock, the health secretary. Mr Cameron also sent text messages to Rishi Sunak, the chancellor, as the company faced imminent insolvency and unsuccessfully sought a Bank of England loan facility aimed at helping companies to withstand the Covid crisis.

‘The revelations of Mr Cameron’s lobbying prompted the disclosure this week that Bill Crothers, a former head of government procurement, had combined this civil service role with working for Greensill…

“These are extraordinary revelations. It is little wonder that Lord Pickles, who heads the official Advisory Committee on Business Appointments (Acoba), expressed incredulity to MPs yesterday [15 April] about the lack of boundaries between public service and commerce” (‘The Times view on the Greensill affair and the civil service: Beyond the Boundaries’, 16 April 2021).

It is well-established that Greensill, despite all Cameron’s efforts, did not succeed in his main objective which was to be included in the Chancellor’s emergency Covid loan scheme known as the Covid Corporate Financing Facility (CCFF), designed to support blue chip industries through the pandemic. The CCFF “was a way for the state to lend money to blue-chip companies, not to a financial services start-up. Charles Roxburgh, the Treasury’s second most senior official, spoke for Sunak [the Chancellor], having ‘obtained a view’ directly from the chancellor. The conclusion was firm: ‘We cannot consider your request further.’

“However, Cameron would not take no for an answer. He began a lobbying campaign that soon secured Greensill special access to the Treasury’s most senior officials. The financier was able to pitch his ideas and exert his charms at the highest levels of government for months” (Caroline Wheeler and Gabriel Pogrund, ‘David Cameron spent two months browbeating Rishi Sunak’s officials’, Sunday Times, 11 April 2021). In fact, “The privileged access which Greensill, a senior adviser to Cameron in Downing St from 2012 to 2016, obtained to the Treasury’s two most senior officials as he fought for this reform [of the rules relating to CCFF] has raised eyebrows. Time with permanent secretaries and their deputies is known to be severely limited. Greensill had ten meetings in 2020” (Dominic Kennedy and Oliver Wright, ‘Treasury officials sought to change the rules for Greensill Capital’, The Times, 10 April 2021). Even Sunak himself was drawn into the exercise of making sure that Greensill got hearing after hearing for his proposals and amended proposals that on the face of it should have been summarily dismissed for not fulfilling the required criteria. In the end, however, despite all the browbeating, the answer was still NO.

Nevertheless, Greensill, thanks it seems to Cameron’s successful lobbying of Health Secretary Matt Hancock and others, did not by any means go away empty handed:

“As administrators wind up what is left of Greensill’s empire, questions remain about how the company was able to get so close to the public sector, securing, between 2018 and last month, contracts to pay NHS pharmacies and staff and also become an accredited lender under another Sunak scheme, the Coronavirus Large Business Interruption Loan Scheme. The government has been asked to explain how Greensill was able to lend £400 million in taxpayer-backed money to one steel empire under that scheme, when the maximum to any one group was meant to be £50 million” (Caroline Wheeler and Gabriel Pogrund, op.cit.).

These sweeteners, however, were not enough to save him.

Consequences of the Gupta and Greensill insolvencies

There are 35,000 Gupta employees around the world, 7,000 of whom are in Britain, working in core industries. They face redundancy and the businesses they work for face closure. There may be a few enterprises that can be sold and that might then be kept functioning by their buyers, but most are no more marketable as going concerns than they were when Gupta was able to buy them precisely because of their very unprofitability.

There is some talk of Gupta’s largest UK operation, Liberty Steel, being taken into public ownership, with MPs Steve Kinnock and Miriam Cates, both representing steel-making constituencies, forcefully making the case for this in The Times:

“…Politicians, academics, journalists and commentators are recognising UK steelmaking for what it is: a 21st-century industry that forms the backbone of our manufacturing sector and underpins our prosperity as a nation.

“The Conservatives won the 2019 election on a promise to ‘level up’ Britain, acknowledging that for too many years Britain’s industrial communities have been neglected. For too long our future has been viewed through the lens of cheap imports and hyper-globalisation. Both Labour and the Conservatives now recognise the key role that steel can play in delivering well paid jobs and economic prosperity across the UK.

“But steel is about so much more than just jobs. The pandemic has led us to rethink which industries are critical to guarding against economic shocks. Steel is critical to our economic and national security. After all, every military vehicle built, every major infrastructure project commissioned, and every kitchen fitted and kitted will require steel. It makes sense for us to want as much of that steel as possible to be produced in the UK, supporting British jobs. It is clear that over-reliance on imports in times of crisis is a real danger.

“Then there is the recognition of the vital role of the steel industry in tackling another major global challenge – climate change. Steel will play a critical role in greening our economy by building the electric cars of the future and the technology to harness solar, wind and tidal power.

“It is of course far greener to make steel for UK projects here in the UK. Domestically produced steel has half the carbon footprint of Chinese imports, and importing steel thousands of miles means increasing carbon emissions while the UK steel industry is committed to moving further and faster in going carbon neutral. …

“IPPR North’s newly published report Forging the Future focuses on decarbonisation within the steel industry and recognises that there will be no zero-carbon economy without a strong low-carbon UK steel sector” (‘Time to step up and save our steel industry’, 19 April 2021).

It is of course naïve, or more probably disingenuous, to imagine that the billionaires who rule the capitalist world would be prepared to sacrifice one iota of their profits either so that workers could have well-paid jobs, or to support local industry, and even less out of any interest in saving the planet. Unless a strong case is made for the likelihood of their competitiveness and therefore profits either being increased, or, in the event of inaction being seriously threatened, in the reasonably short term, any such ‘common sense’ pleas, whether made by MPs or anyone else, will fall on deaf ears and nothing meaningful will be done. It is possible that governments with their eyes on the next election will risk nationalising some of these industries for taxpayers to support for a while as loss-making concerns, but this is unlikely to lead to any long-term respite. Not only in Britain but all over the world where the Gupta empire extended, governments are facing the need to make similar decisions, just as the Covid emergency has stretched their borrowing capacity to unprecedented extents.

As ever, the proletariat cannot but gape open-mouthed at the absurdity of the capitalist system which routinely allows the fate of essential industries and millions of workers to be determined by the foolish, the fraudulent, the profligate and the rapacious in search of the quick buck. All essential industries, both heavy and light, as indeed all essential utilities and service providers should be state-owned by states managed and controlled by the working class, having not the slightest interest in profit but only in the wellbeing of the masses of the people. Only the working class is able to deploy these resources to serve the interests of the people rather than to allow these to take second place to the supreme interest of the capitalist world – the interest of the profits of money-grubbing billionaires.

Comments are closed, but trackbacks and pingbacks are open.